Looking for the most important DEA Fund Scheme MCQs for your upcoming exams? We have analyzed past papers for Bank Promotion Exams to bring you the 12 most expected questions. Take the live test, review the blueprint, and master the core concepts.

📚 Interactive Question Bank

Select a question to view the expert explanation and answer.

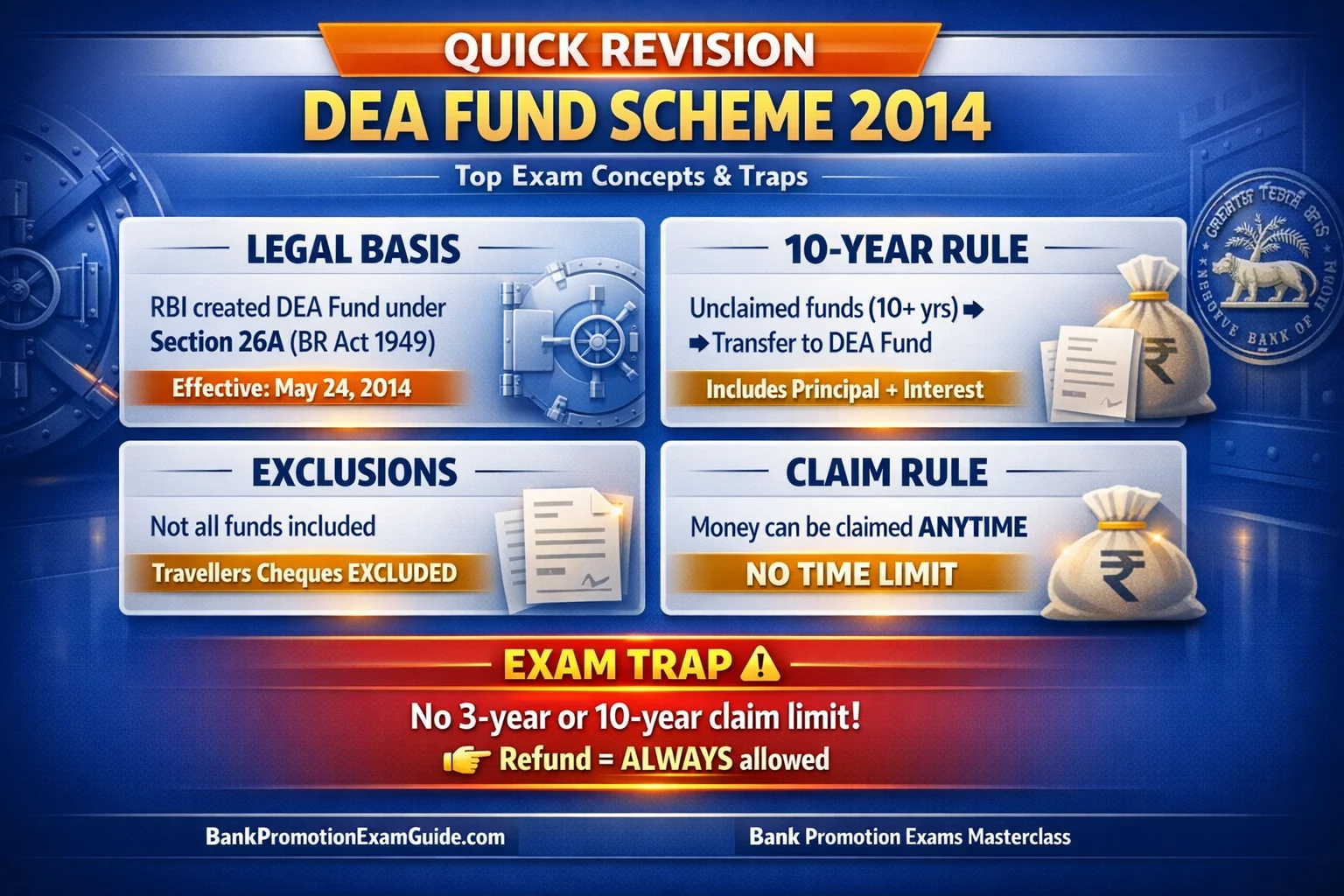

✅ | DEA Fund – Establishment & Legal Basis

Q1Under which section of the Banking Regulation (BR) Act, 1949, was the Reserve Bank of India (RBI) empowered to formulate "The Depositor Education and Awareness Fund (DEA Fund) Scheme, 2014"?Q2Which of the following types of amounts are credited to the DEA Fund, if they remain unclaimed for 10 years or more?Q3What is the minimum period an amount must remain unclaimed or a deposit account must be inoperative, for the funds to be transferred to the Depositor Education and Awareness (DEA) Fund?Q4When did the Depositor Education and Awareness (DEA) Fund Scheme, 2014, come into effect?

✅ | Scope and Fund Transfer Rules

Q5After remaining unclaimed for 10 years or more, all of the following amounts are credited to the DEA Fund EXCEPT:Q6When are banks required to transfer the credit balances from 10-year inoperative or unclaimed accounts to the DEA Fund?Q7When a bank transfers the amount from a 10-year unclaimed deposit to the DEA Fund, what happens to the interest accrued on that deposit?

✅ | Claims Process and Liquidation Rules

Q8Consider the following statements:Q9There is ...... prescribed in the Scheme for a customer/depositor for claiming a refund from the DEA Fund.Q10In the event that a bank is under liquidation, who should a depositor approach to claim their unclaimed deposit amount that was previously transferred to the DEA Fund?Q11For a bank under liquidation, if a customer's deposit was covered by DICGC at the time of transfer to the DEA Fund, how does the Liquidator handle the claim (up to the insured amount)?Q12For a bank under liquidation, if a DICGC-insured deposit claim (e.g., 6 lakh) is more than the DICGC insurance cover (e.g., 5 lakh), how is the amount in excess of the cover (e.g., 1 lakh) handled?

Page 1 of 1 (12 Total Questions)

💬 Frequently Asked Questions

Why are DEA Fund Scheme MCQs critical for Bank Promotion Exams?

It is a consistently high-scoring area. Examiners frequently repeat core concepts regarding the 10-year rule and Section 26A BR Act compliance.

Does this mock test cover the full syllabus?

Yes, these questions target the most highly-weighted concepts found in previous years’ papers regarding Unclaimed Deposits and claim procedures.

What are the most repeated topics?

Based on our blueprint, the Claims Process during liquidation and the exact mechanisms of a Liquidator DICGC Claim carry the highest weightage.

📺 Video Masterclass

⏱️ Jump to Topic: